Cinderella and her stepsisters have a retirement plan.

The brief (less than 2 minutes) video linked below offers a different take on the story of Cinderella and her stepsisters. It illustrates an example of what is referred to as sequence of returns risk. After you view the video please read through the situation, result and conclusions below.

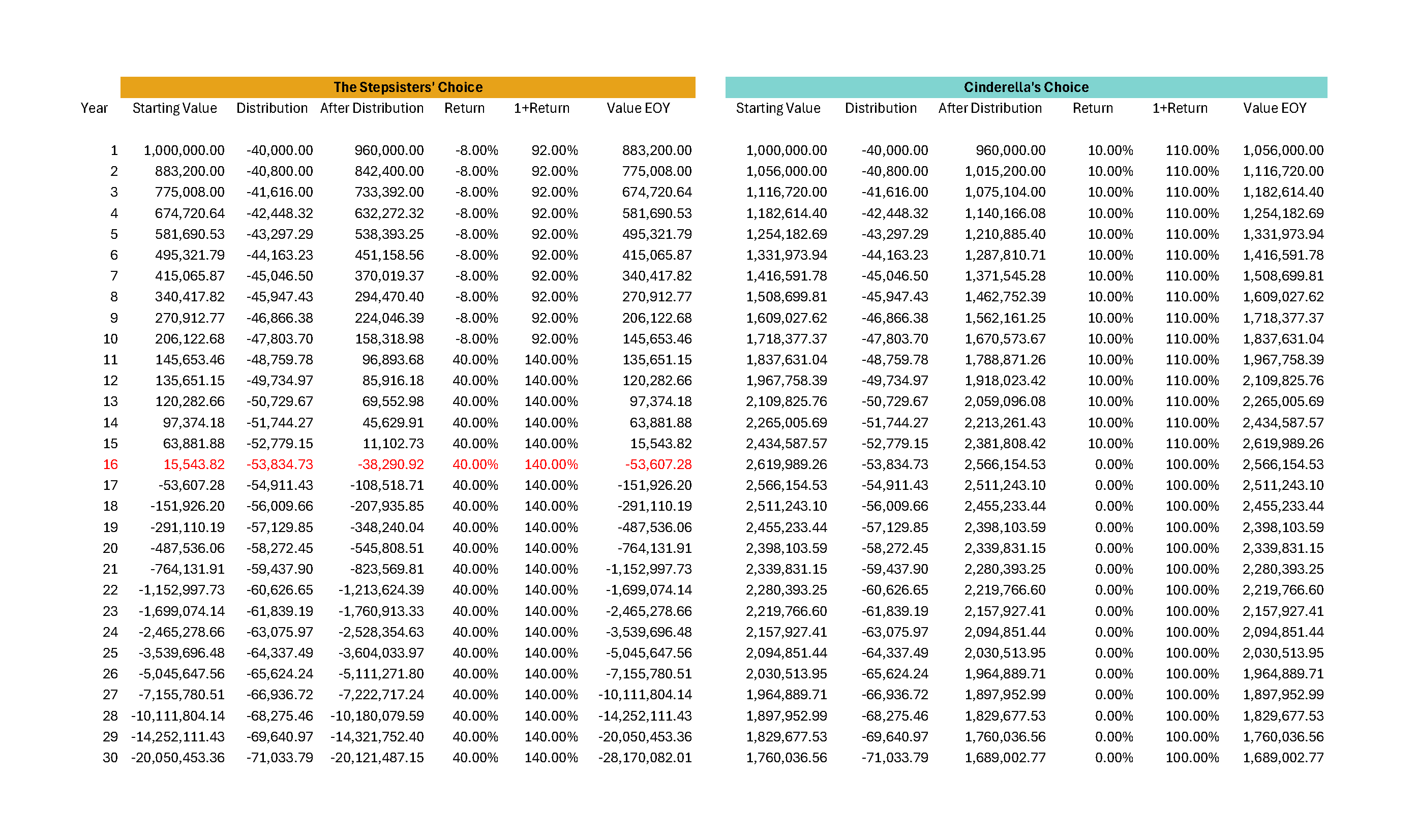

The situation:

At age 65 Cinderella and her stepsisters had no money or assets. Apparently, Cinderella’s relationship with the prince she met at the ball did not last, and the stepsisters were never able to hold steady jobs due to their less than charming personalities. Fortunately, before he died the sisters’ long-lost father had set up a trust fund for Cinderella and her stepsisters. Each was given $1,000,000 to meet their financial needs during the remainder of their lives. Each sister required $40,000 per year to meet expenses. Because of inflation their expenses increased each year by 2%.

At that time there were only two investments to choose from.

Investment A would lose value during the early years, namely 8% per year for the first 10 years. However, this investment would gain 40% each year for the next 20 years resulting in an average annual return over the girls’ 30-year life expectancies of 22% per year. This is the investment chosen by the stepsisters.

Cinderella chose investment B which would gain 10% per year for the first 15 years but have no growth thereafter. The average annual return for this investment would be just 4.7% per year.

The result:

The stepsisters ran out of money in the 16th year. Cinderella did not run out of money. (Note: The creator of the video/story indicates that the stepsisters ran out of money in the 19th year, not the 16th. I believe I know where he made his mistake, but that isn’t important just now.) The table below models the specific cash flows for the sisters during their retirement periods. Click on the table to enlarge it. Use your browser back button (or for Windows users alt+left arrow) to revert to the prior size.

The conclusion:

The issue considered here is often referred to as sequence of returns risk, which recognizes that with regard to retirement planning situations the investment with the greatest average return is not necessarily the one most likely to provide the best chance of retirement success.

In reality the variability of investment returns is not usually as extreme as what is specified in the sisters’ example. Still, those who have studied sequence of returns risk have shown that the following conclusions can be drawn:

- In general, it is better to have positive returns early on.

- Less volatility will likely increase the probability of success.

These generalizations should be considered when developing an investment strategy.

How can I account for sequence of returns risk?

Financial Planning Associates, Inc. maintains securely linked professional level tools for modeling asset values, cash flows, investment returns, volatility, sequence of returns risk, life expectancies, inflation, etc. Probability of Success calculations based on 1000 trial sequences are included among the important reports available to our clients.

Our clients have the data to make informed decisions regarding their retirement goals.