In this blogpost, in addition to discussing the paperless office question I will share some information regarding inflation, techknowledgy¹ and the continuing value of investment diversification. But, first a brief update for our asset management clients follows below:

Midway through the 4th quarter of 2015 our investment clients are all experiencing positive growth.

The paperless office has been a dream of many a paper shuffler over recent decades. With the advent of the computing machine, with its word processing capabilities some have predicted the demise of paper as a requirement to do business. That hasn’t happened yet. I came across a piece published in 2008 concerning the paperless office dream which postulates that, “The relationship between the paper and electronic worlds is more complicated than we first thought.” The full article is pretty interesting and can be found here. The final thought stated in the piece is that perhaps eventually “computers will become paper.” This may happen, but for the moment I would like to mention a few observations about the state of business, and paper, in 2015.

Some businesses, especially those established long ago find it difficult to move from their legacy systems, highly dependent on paper flow, to newer, less paper dependent systems simply because the disruption(s) associated with change(s) would affect current profit. In other cases loss of profit might not be the problem, just inertia. In spite of inertia and loss of immediate profit most enterprises will find it necessary eventually to adopt new technologies if they are to survive. And, newer businesses often have an advantage as a result of not having to “fix” the problem of older, less efficient systems.

So, paper has not (yet) disappeared, but today businesses accomplish much, much more with far less paper than would be required absent the digital technologies now available. I will mention just three examples. Today, when someone sees a doctor he, or she is likely to leave with a readable document (as opposed to doctor scribble) summarizing the important details of the visit. True, today the document is likely to be made of paper, but the same information is also likely to be available online in a secure account accessible by the patient at any time. And before long the summary will likely not be written on paper at all, just posted or downloaded for the benefit of the patient. If you take a moment to consider all of the efficiencies associated with this arrangement versus the traditional paper-based system you will see that much greater efficiency is possible, and therefore much lower cost. (Ex: Less misunderstanding of instructions, etc., so fewer call backs to clarify misunderstandings, fewer mistakes made resulting in fewer expensive remedial treatments and fewer lawsuits, etc., etc.)

There are countless other examples of business efficiencies resulting from the use of digital technologies to transmit information instead of paper. I have a lot of personal experience with this second example – financial planning and investment management. In the financial planning biz we used to send our clients home with a large notebook of reports for their review and for implementation of a strategic plan. Some of us jokingly referred to this process as “planning by the pound.” The best financial plans were quite heavy. Hewlett Packard was happy. And clients usually equated volume with quality. Making changes to the plan was a major trauma. Today, we can offer much, much better planning assistance with little or no paper. Changes are made immediately and easily. Reports are posted securely for clients, and advisers to view, discuss and revise at any convenient time. For my office, the dream of being paperless is very nearly a reality. Some of the drawers in our filing cabinets are now home to office snacks and old paperweights.

The final example that I would like to mention has to do with our old washing machine. A couple of weeks ago it failed. We called an appliance repair company and they sent a man out. When he had completed his assessment he handed me his tablet computer for payment via my signature. A receipt was immediately emailed to me. No paper. And I’m quite certain that all of the relevant data required by his company to understand and maintain their relationship with my household was also immediately stored and easily available to management at any time.

By the way, his assessment was that we needed a new washer.

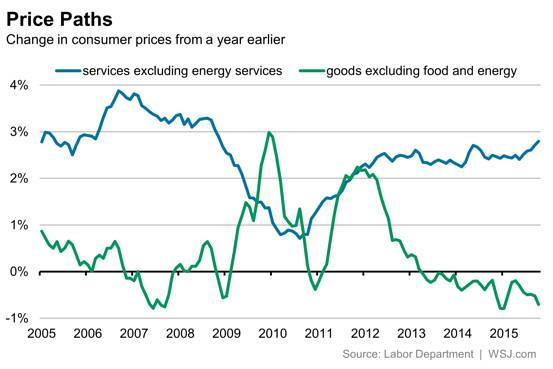

So, given that technological efficiencies are happening all around us, what does that mean for economic growth and inflation? In my opinion, (To my regular readers this will sound familiar.) one result will be that inflation will be mitigated. And, in spite of an abundance of warnings from smart economists and not-necessarily-smart talking heads and politicians that high inflation must follow the stimulative Federal Reserve policies of the past six years it still hasn’t happened. In times past they would perhaps have been right, but our time is not exactly like times past. Some things really are different this time. Automation and new efficiencies are deflationary. As well, new efficiencies bode ill for “full” employment and increasing wages, and in some cases corporate profits. The attached image entitled “Price Paths” conveys information concerning the change in consumer prices for recent years as of October 31st. It comes from today’s (Nov. 17) Wall Street Journal, using data from the Department of Labor. I have lifted some bits from the text accompanying the chart:

So, given that technological efficiencies are happening all around us, what does that mean for economic growth and inflation? In my opinion, (To my regular readers this will sound familiar.) one result will be that inflation will be mitigated. And, in spite of an abundance of warnings from smart economists and not-necessarily-smart talking heads and politicians that high inflation must follow the stimulative Federal Reserve policies of the past six years it still hasn’t happened. In times past they would perhaps have been right, but our time is not exactly like times past. Some things really are different this time. Automation and new efficiencies are deflationary. As well, new efficiencies bode ill for “full” employment and increasing wages, and in some cases corporate profits. The attached image entitled “Price Paths” conveys information concerning the change in consumer prices for recent years as of October 31st. It comes from today’s (Nov. 17) Wall Street Journal, using data from the Department of Labor. I have lifted some bits from the text accompanying the chart:

“…the Federal Reserve’s preferred measure of core prices remained up just 1.3% on the year…Core goods, heavily exposed to dollar strength² and overseas economic weakness, were down 0.7% in October from a year earlier…And companies that make and sell goods, like manufacturers and retailers, are losing sales to deflation…”

Prices for goods (in general) have been falling, and even price increases for services remain below 3%. The phrase “do more with less” is ubiquitous, and businesses are doing more. With less.

And speaking of technological efficiencies, we have installed a new system for making appointments quickly and easily. If you would like to make an appointment with yours truly you just go to our website (fpai.net) and click the “Contact Us” link from the menu bar across the top of the page. Then click the “Schedule Now” icon and follow the prompts. The system integrates with my calendar so that only open dates and times are shown as available. You can schedule face-to-face meetings, or phone or video meetings. Once you have scheduled a meeting you will be sent an email with details which can then be saved to your calendar. And you will be sent an email reminder of the meeting 24 hours in advance of the meeting time, and also one hour before the meeting time. Go ahead. Give it a try.

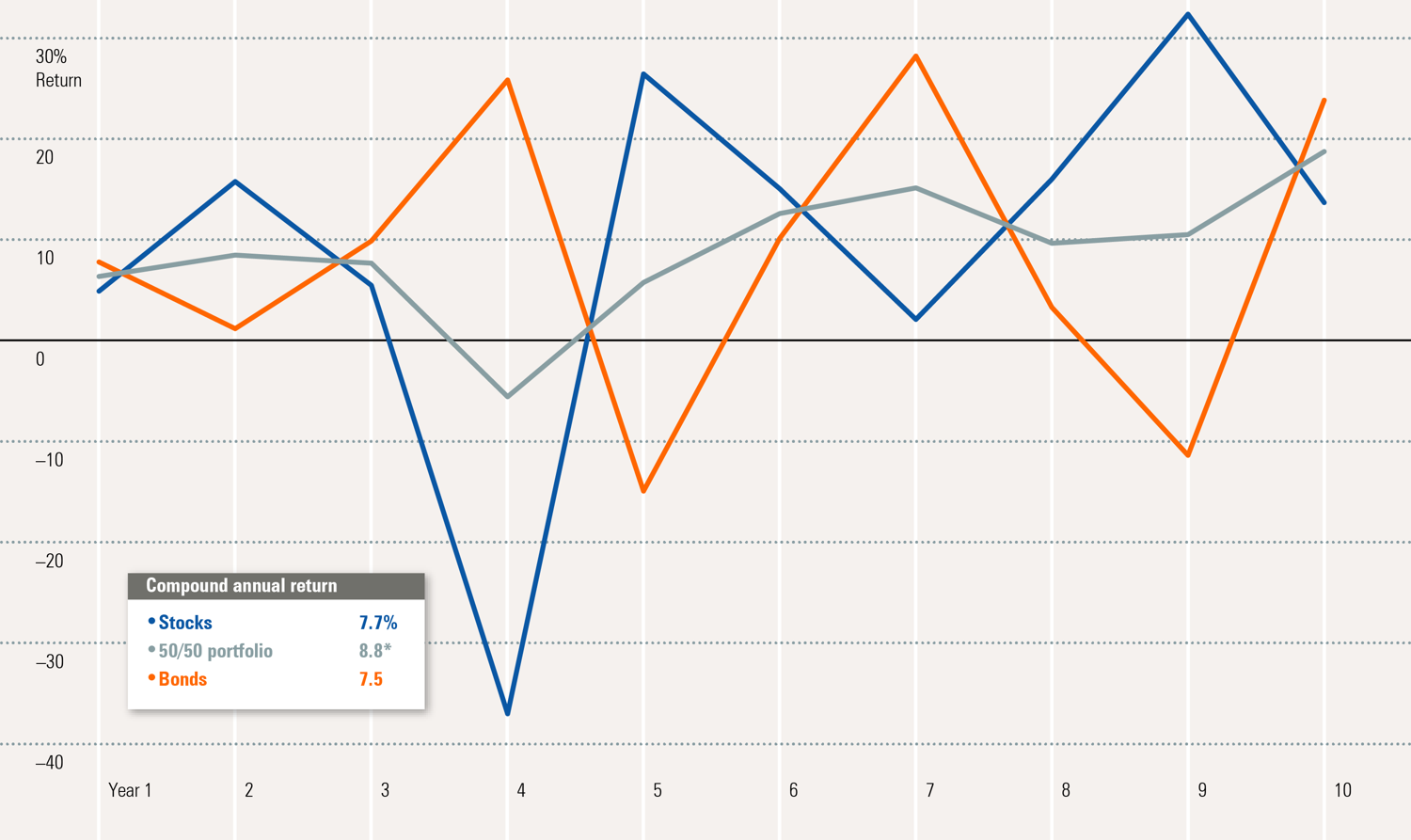

It comes up during asset management review meetings with our clients, the question of whether diversification of assets is (still) the best approach to managing a portfolio. I believe that it is. Investment markets remain pretty doggone efficient most of the time.

Stock and Bond Returns, 2005 – 2014

The respected investor, John Bogle, founder of The Vanguard Group/Vanguard Funds once said that, “Markets are efficient, except when they’re not.” Of course, the problem is determining when they are not. So, assuming that it is impossible to consistently determine when markets are not efficient the prudent investor does well to continue to remain broadly and (at least somewhat) efficiently diversified. A discussion of the distinction between a theoretically efficient portfolio and a somewhat efficient portfolio will be a topic for another time.

As you can see from the accompanying graphic, during the recent past (2005 through 2014) stock and bond values were quite volatile. The total compound annual return of stocks during the period was 7.7%, and the return for bonds was 7.5%. A portfolio of 50% stocks and 50% bonds was significantly less volatile than either stocks or bonds. And yet, the annualized return for the 50/50 portfolio was higher than either of the constituent members alone. This is possible because this hypothetical portfolio was rebalanced annually, which resulted in buying each asset at a relatively low price.

To implement a diversification strategy the investor must decide how and when to rebalance the portfolio. There are many possibilities. One strategy would be to never rebalance. Another would be to rebalance annually, or quarterly or monthly, and still another to rebalance when any asset moves more than a certain amount above or below its target percentage. The target percentage strategy requires the investor to choose to base disparities on the relationship to the total portfolio, or the specific asset value, and to determine whether the various “bands” should be symmetrical (the same value for gains as losses). The investor must also decide whether and when to “interfere” with the rebalancing schedule based on current and/or anticipated market conditions, trading costs and tax consequences.

Finally, it should be noted that strategic portfolio rebalancing can result in a higher total return, but often does not. The primary benefit is managing (limiting) portfolio risk.

Comments and referrals always welcome!

Do you have RMDs to distribute? Now is the time. Call us if you have questions. Or click the link above to make a phone, video or office appointment.

Thought for the day: Time is what keeps things from happening all at once.