Economists and psychologists have conducted studies to determine whether investors always act rationally. They don’t. A number of persistent patterns of irrational investor behavior have been identified, including overconfidence, hindsight bias, short-term focus, regret, mental accounting and the hot-hand fallacy. We all tend to make these mental mistakes but can avoid them once we become aware.

With this writing we will consider the irrational investor behavior referred to as short-term focus, which occurs when an investor attributes too much significance to short-term portfolio volatility. As a result, the investor may then make decisions that work against his long-term interests.

(Note: Clicking on the images shown below will increase the size. After viewing the larger image, you should click the back arrow on your browser to return.)

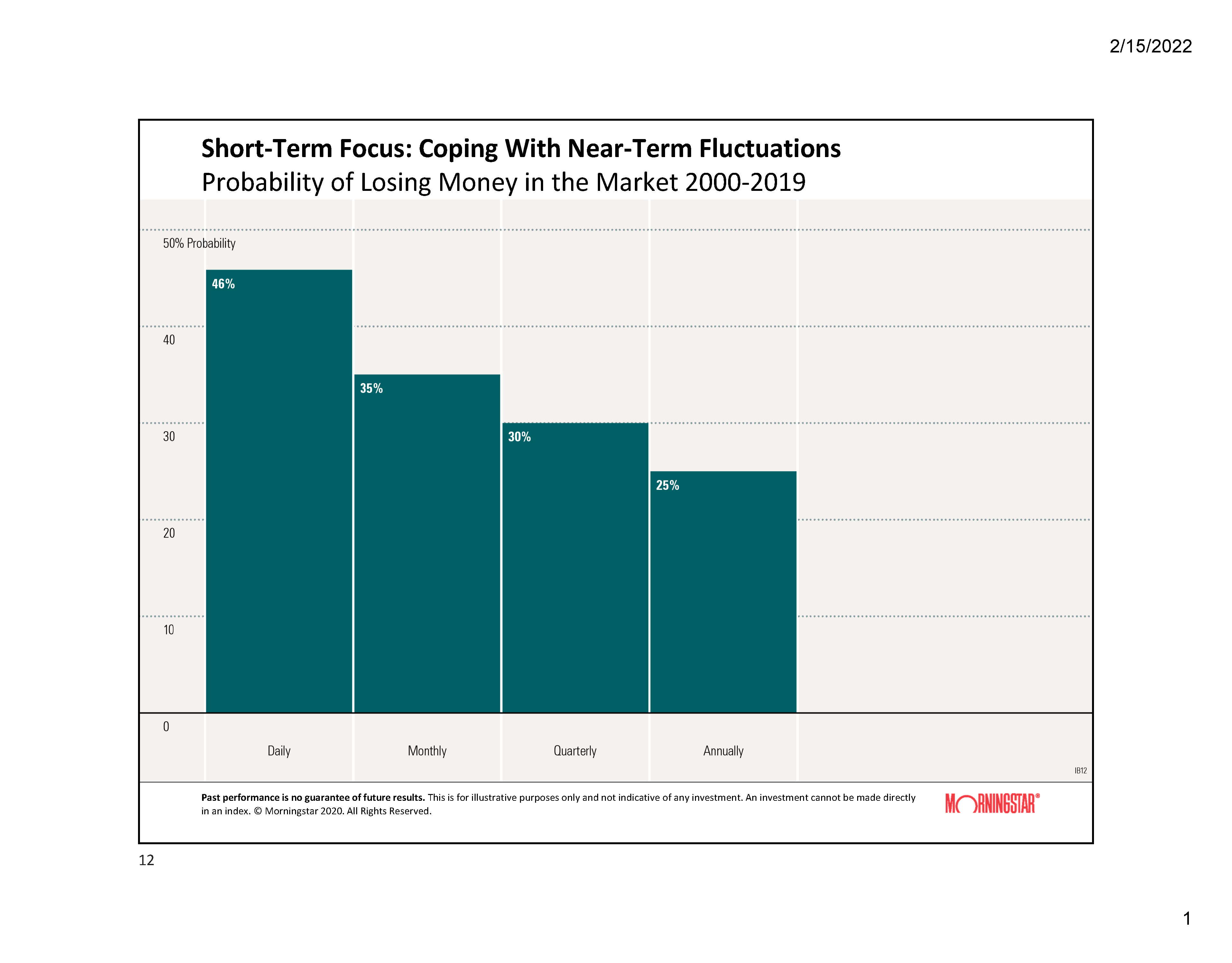

The image below illustrates that stock market fluctuations tend toward positive results over time. During the twenty-year period shown an index of US-based large capitalization common stocks was more than twice as likely to lose value during any given day than over any twelve-month period. It should be noted that the trend, although not illustrated here does continue: positive stock market returns become more likely as the holding period increases.

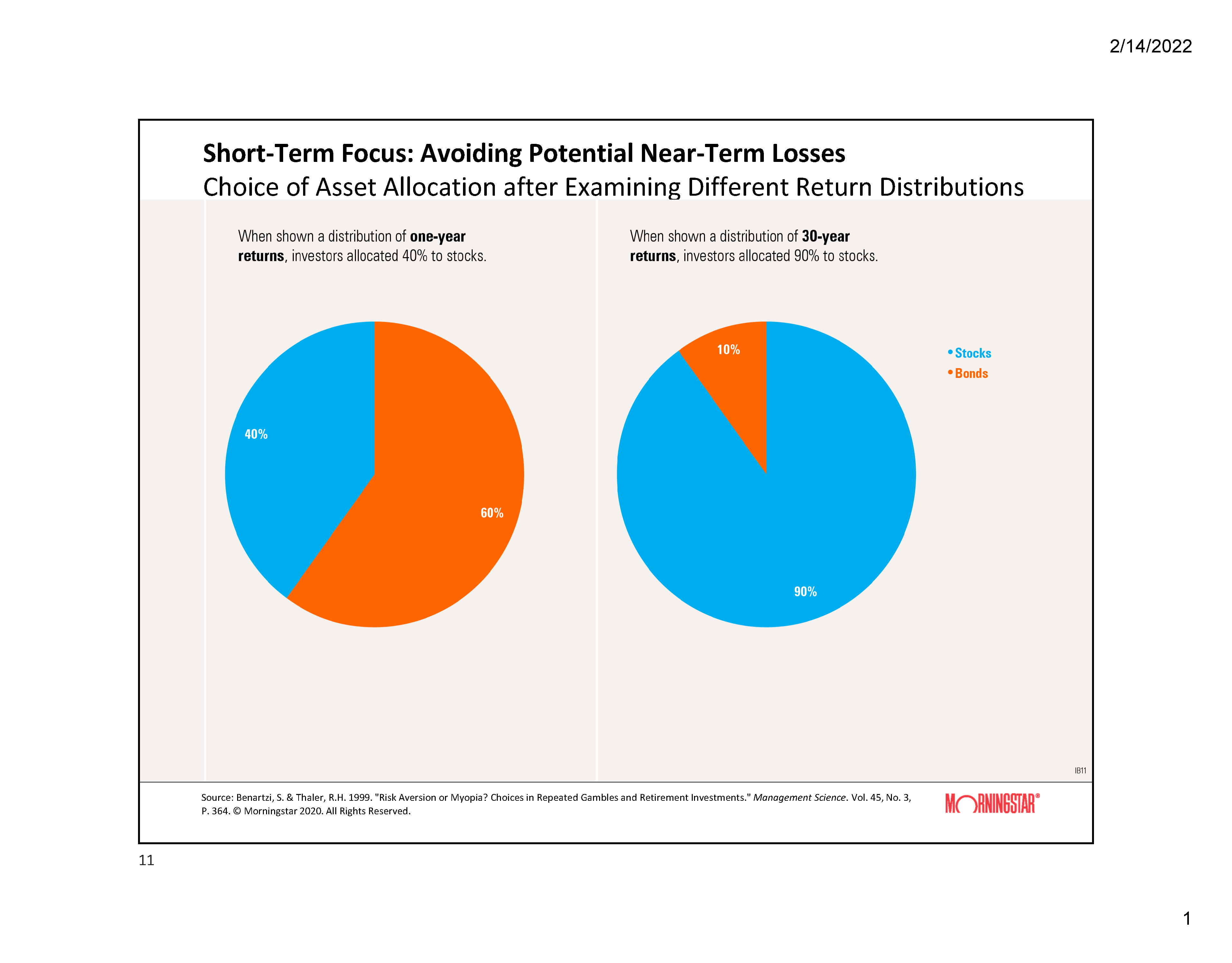

Shlomo Benartzi and Richard Thaler, professors at the Anderson School at UCLA and the University of Chicago, respectively, studied a group of defined contribution plan participants. One group was shown a distribution of one-year returns for both stocks and bonds. The other group was shown a distribution of 30-year returns. The results found that the group looking at the distribution of one-year returns allocated their portfolios much more conservatively: 60% to bonds and 40% to stocks. In contrast, the group that saw the 30-year return distribution allocated their portfolios more aggressively: 10% to bonds and 90% to stocks. Exposure to frequency of returns tends to affect an investor’s tolerance for risk.

The moral of this story is: a rational long-term equity investor should avoid having a short-term focus.

Inflation: Entrenched or Transitory?

Many economists were surprised recently when the latest inflation readings were higher than expected. Higher inflation will lead to higher interest rates as the Fed seeks to move the rate back to a more acceptable level. Higher interest rates are likely to result in lower corporate profits and therefore lower stock values, at least for a time. So, the question of whether higher inflation is likely to become entrenched, or merely temporary is relevant to investors. Some economists are convinced and concerned that the evidence suggests entrenchment and therefore interest rate increases should be sooner and greater. Others are less concerned, and hopeful that the rate of inflation will return to the 2% to 3% range within months without extreme Fed intervention. If the latter view proves correct stock prices will likely recover fairly quickly. Otherwise, equity pain will likely last longer. A bit of evidence supporting the hopeful camp is included below.

John Rekenthaler is a member of the Morningstar research department. He recently observed that certain assets which would be expected to gain value during inflationary times have not done so. Excerpted below are some of his conclusions:

…The problem doesn’t lie with the assets…The reason for the uninspiring performance of the inflation hedges thus lies elsewhere, outside the investments themselves. One possible explanation is that current inflation is a mirage. Not to say, of course, that the Bureau of Labor Statistics cooked the numbers (government bodies are not in the habit of spoiling their own reports), but instead that the increase is only temporary. When the global supply chain becomes unstuck, inflation will diminish.

…The bond market has treated, and continues to treat, today’s inflation as a mirage. The yield on 30-year Treasuries has declined since May 12, 2021. (Yes, it has.) The public may regard inflation as a headache, but not bond investors. They see no need to hedge against inflation that will not persist.

The upshot: Inflation hedges disappointed because the financial markets aren’t (yet) convinced that inflation is here to stay…

Thanks for reading.